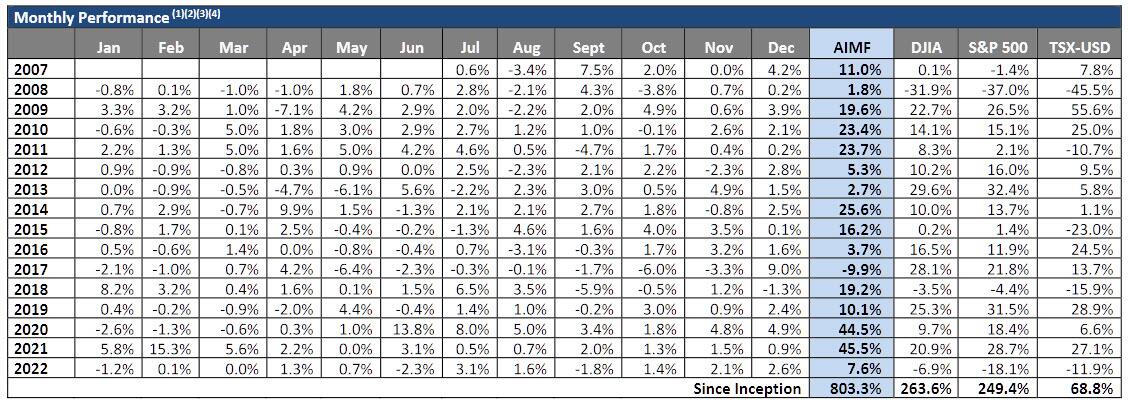

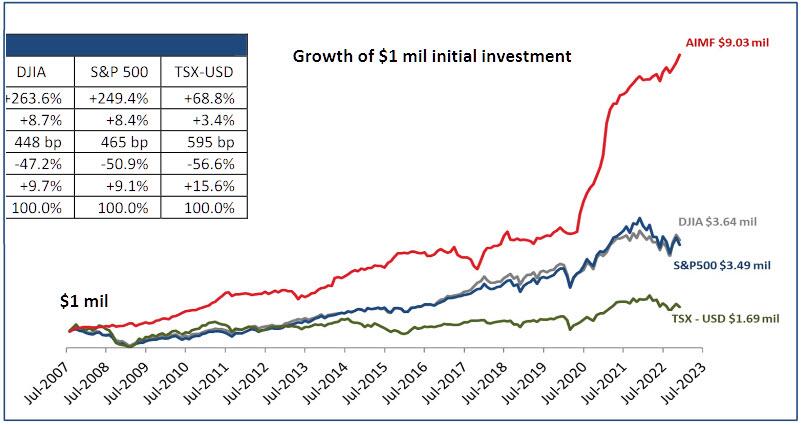

“…One hedge fund which we were unfamiliar with, yet which has posted solid returns not just in 2022 but also in prior years, is the $1.6 billion Anson Funds. What we find most impressive, is not so much the fund’s 2022 return (where it’s 7.6% return still made the top 5%-ile of all funds for the year) but its performance in the prior two years, when it posted 40%+ profits in both 2020 and 2021. Just as remarkable: in its 15 year history, the fund has had just one down year (no, it wasn’t 2008)…

… allowing it to generate a 800% total return since 2007.

…Among the fund’s short positions are what it dubs “Retail momentum and stock promotion”, as well as high valuation on poor businesses or fads, and companies that exhibit fraudulent behavior, while longs are companies with strong secular tailwinds, as well as positive price momentum and attractive valuations.”

Anson Funds Chief Investment Officer Moez Kassam quoted in Reuters story on recent market strength.

“What I think you’re seeing is renewed investor enthusiasm fueled by those who see that beautiful light at the end of what has been a very dark tunnel. And there has been so much money on the sidelines that is rushing back into the markets and waiting to get back into the action”

Once again, our flagship fund, Anson Investments (AIMF), was listed as a Top 10 Hedge Fund by BarclayHedge in its Barclay Managed Funds Report.

For the 1st Quarter 2022, AIMF ranked 4th among Equity Long/Short funds in the BarclayHedge database in three year compound returns (from 1-Apr-2019 through 31-Mar-2022), returning an average of 32.17% net of all fees on an annual basis over the period.

Among the Top 10 Equity Long/Short funds in the ranking, AIMF had the highest AUM, the highest Sharpe Ratio (2.43%), the lowest drawdown (4%), and the third lowest correlation to the S&P 500 Index.

Our flagship fund, Anson Investments (AIMF), was listed as a Top 10 Hedge Fund by BarclayHedge in the 4th Quarter 2021 issue of the Barclay Managed Funds Report (for the second year in a row).

AIMF ranked 3rd among Equity Long/Short funds in the BarclayHedge database in three year compound returns (from 1-Jan-2019 through 31-Dec-2021), returning an average of 32.36% net of all fees on an annual basis over the period.

Among the Top 10 Equity Long/Short funds in the ranking, AIMF had the highest Sharpe Ratio, the lowest drawdown, and the lowest correlation to the S&P 500 Index.

“With the rise of the retail investor and the extreme moves that so-called ‘meme stocks’ have experienced, prudent risk management processes have become increasingly important to ensure that market actors have enough protection against downside scenarios, which can emerge with alarming speed.”

Strategies

To achieve its record-breaking performance over the last two years, Anson Funds has relied upon the diversity and versatility of its multi‐strategy approach. Anson Funds utilises several different investment strategies that thrive during different market environments – longs (tactical equity and REITs), shorts (momentum reversals and fundamental shorts) and opportunistic (structured financings, SPACs & catalyst driven investing).

Kassam says:

“We have been able to harness the opportunities available to us in the overall market environment that manifests in any given period of time. Then, as market sentiment changes, we have successfully been able to pass the baton on to other strategies that are better suited for the new reality. This sounds easy to do retrospectively, but it requires significant skill and discipline to execute in real-time when market signals are still clouded with significant statistical noise.”

Each of Anson Funds’ sub-strategies generated strong returns during the past year, but some performed better at different times of the year than others.

Best Equity Hedge Fund – Secret to success

Kassam adds:

“The secret to our success is that we are market agnostic. We invest enormous resources, both in terms of human capital and of machine intelligence, to understand the directional contours of the market at any given time, and then adjust our investment approach accordingly.”

Anson Funds has learned that markets, and individual stocks, can act irrationally for long periods of time due to the combination of extremely loose fiscal and monetary policy, and the rise of the retail investor. Firms need to be willing to take losses and move when things don’t go their way.

Looking ahead

Going forward, Anson Funds believes that more volatility is in store for markets. “Many new funds have juiced returns in this period through some combination of leverage and extreme concentration,” Kassam said. “That kind of strategy works until it doesn’t, and then the bottom can fall out of a fund’s performance.” The key, he believes, is to play the long game. “Our investors are looking to compound wealth over the long-term. This is our responsibility as stewards of their capital.”

Anson Funds CIO Moez Kassam comments in Financial Times story.

The market has seen the share prices of various companies surge to unbelievable levels in 2021, fueled by the efforts of “meme stock armies”.

Losses inflicted by retail investors have proved a rude awakening to hedge funds, which had just enjoyed a banner year in 2020 making their biggest gains since the aftermath of the financial crisis, according to HFR. Some funds are considering taking a greater number of smaller short positions to cut down on the potential losses a single stock can cause, say industry insiders.

Financial Times 24-June-2021

Moez shares some of his thoughts on the topic with the Financial Times.

Our flagship fund, Anson Investments (AIMF) was listed as a Top 10 Hedge Fund by BarclayHedge in the 4th Quarter 2020 issue of the Barclay Managed Funds Report.

AIMF ranked 7th among Equity Long/Short funds in three year compound annual returns for the period 1-Jan-2018 to 31-Dec-2021, returning an average of 23.85% net of all fees on an annual basis over the period.

Among the Top 10 Equity Long/Short funds in the ranking, AIMF had the second highest Sharpe Ratio, the second lowest drawdown, and the lowest correlation versus the S&P 500 Index over the period.

Anson Funds, which returned more than double the S&P 500 in 2020, recommends skipping the fundamentals and focusing on sentiment as retail traders take an outsized role in the market. That is what pushed Anson to trade on themes and stocks popular with individual investors last year, including positions in Apollo Healthcare Corp., Genius Brands International Inc. and Hertz Global Holdings Inc.

Those investments helped drive Anson to a 44% gain last year, bringing its total assets under management to C$1.2 billion ($944 million). By comparison, the S&P 500 returned 18% while peers in the Scotiabank Canadian Hedge Fund Index, which tracks funds that manage at least C$15 million, added 6.2%.

“People have to understand stocks don’t really move on fundamentals in the short term, rather they move on the sentiment. A whole new class of investors has emerged, empowered by new technology platforms such as Robinhood and becoming significant drivers of the excitement in the market.”

Investing—like life itself—has always meant dealing with uncertainty; yet the first half of 2020 has forced people to deal with far more uncertainty than usual. There is always uncertainty about the distant future. The issue today is the incredible uncertainty regarding even the near future: the days, weeks, and months directly ahead of us.

In their recently published mid-year update, JP Morgan made noted that “the Covid-19 crash has been a stark reminder to expect the unexpected”. Very true. The same report also pointed out that “…at the start of 2020, very few experts predicted that within a few months a new pandemic would cause the global economy to effectively shut down and equity markets to go through one of the most severe bear markets in history, and then rally over 40% in 50 days from the bottom.” Uncertainty remains the biggest issue we face for the rest of 2020 and beyond

Without a doubt, 2020 will be a year to remember

Early in 2020, dreadful pandemic, the deadly virus, Covid-19, swept the world, initially identified by doctors in the Chinese city of Wuhan; then the virus spread west with the sun–first to Southern Europe and next to the Americas. By mid-March, before the end of the first quarter, the new virus had already become a global phenomenon.

The initial responses to the deadly virus included a combination of lockdowns, quarantines, work-from-home orders, and business shut downs–all imposed by various government officials scrambling to react to the rapidly-moving humanitarian and public health crises. Following these man-made shutdowns, economies everywhere screeched to a halt, resulting in some of the worst economic numbers since the Great Depression of the 1930s– almost 90 years ago.

As of early July, it appears that the low point has probably passed, and that most economies now seem to be recovering, albeit slowly and unevenly. In the US, this could turn out to be both the sharpest and potentially the shortest recession in the country’s history.

Markets bottomed on March 23, tumbling in just four weeks from all-time highs in late February to new lows, as Covid-19 initially appeared to represent an existential threat.

Central banks and governments reacted swiftly, implementing coordinated monetary and fiscal interventions which led to powerful rallies, pushing markets close to new all time highs. The amount of support injected in response to this crisis is unprecedented; the fiscal, monetary, and political responses to the crisis globally have led to a world awash with liquidity. Much of that liquidity (along with a new wave of optimism given obvious government support) has helped support stock markets, explaining much of the markets’ recent ascent.

Once again, central bankers have promised to do “whatever it takes”. Also, there has been rapid and effective coordination of monetary and fiscal policies between central bankers and government officials, that has become a new normal.

Globally, policymakers have earmarked an astonishing $18 trillion in support, and central banks have cut rates 122 times. This support was designed to help keep business and household cash flows going during the lockdown so as to avoid a devastating wave of bankruptcies and business failures. It seems to be working. In the US, the Federal Reserve fixed the troubling volatility in Treasury markets, and managed to reduce spreads across issuers and maturities by providing a funding backstop for many types of borrowers.

The responses from central banks and governments are likely enough to avoid the worst-case scenario. Still, the path ahead to eventual economic recovery is murky. Business models have been forcibly disrupted. There are questions regarding the long- term viability of the corporate real estate sector. The evolution of the virus remains unknown.

Still, a recovery will come, and may already have started. The contraction has been severe and painful; it will lead to lasting consequences. But there is reason to believe this recovery could happen even faster than the recover after the last global financial crisis, back in 2008.

Powerful rallies in most risk assets…

As John Mauldin recently noted: “The Dow Industrials just closed out their best quarter since 1987, which tends to bode well for stocks. The S&P 500 rose 40% from its March 23 low—its strongest 100-day rally since 1933. And the Nasdaq is the only index that’s up for the year, rising 16% and trading above the 10,000 mark.”

…yet there is still a lot of anger and frustration in the streets

In late May, the death of a man during the course of his arrest by police officers (sadly, a not uncommon occurrence) became the spark that set off weeks of global protests. The fact that the victim was a black man–being arrested by white police officers, in a major American city, and the entire episode was captured on a smartphone video by a bystander–was bad enough. The fact that this event took place during a period of heightened political and social tension, literally added rocket fuel to an already combustible mix that suddenly exploded. People reacted with anger, frustration, and indignation. Mass protests erupted across the USA and eventually in many countries around the world. Sadly, some of the protests turned violent too.

The videotaped death of the suspect was the spark, but the frustrations that fueled social explosion had been accumulating for a while.

At Anson, we have worried about the undercurrent of dissatisfaction for years. When the Occupy Wall Street movement began a few years ago, we were worried that we would soon see “torches and pitchforks” in the streets. We had no idea when the conflagration would light, or what the actual spark would be, but we expected something like this to happen.

We believe that a number of elements have combined to bring forth the anger we see today: the lingering effects of the 2008 Great Financial Crisis, unequal recoveries, the drumbeat of concerns about inequality (whether economic or social), the perceived unfairness of current systems, widely publicized cheating by elites, all combined to fuel anger in the average citizen.

Chamath Palihapitiya, CEO of Social Capital, made some excellent points in his 2019 Annual Letter, comparing our world with the Gilded Age of the late 1800s:

..Imagine a time of incredible economic expansion and wealth creation punctuated by periods of class warfare, strife and political upheaval. During the Gilded Age of the 1870s-1900 we saw all of these: rapid economic growth, wage growth, immigration and expansion of social programs like education with the standardization of primary schools and the emergence of high schools. At the time, the major industry of growth was the railroads which in turn led to technological expansions in factories, mining and farming.

As is the case today, Wall Street played an important role during the Gilded Age as a financial intermediary and financed everything including a bubble in railroads which eventually burst. While this economic expansion was happening, immigrants fled to America in droves and a class division started to emerge with the 1% owning more than 25% of all property and the bottom 50% owning less than 4%.

…Central banks [may not be able] to meaningfully manage inflation, in either direction, but that doesn’t mean [they] won’t continue to drive stock prices higher by unnecessarily cutting rates and flooding markets with money.

…As money gets cheaper, the credit markets continue to expand because CEOs become motivated to artificially boost earnings per share. They do this by buying back stock, seek bad acquisitions, make poor capital allocation decisions or avoid taxes. All enabled by borrowing massive amounts of essentially free money

…The result is a seemingly ever higher stock market. [All of this] has created a complex, interconnected credit-equity bubble. And like other bubbles before it, it will end badly.

Obviously, it is impossible to know how exactly how things will play out, there are so many different opinions and paths possible.

As of early July, the pandemic is clearly still with us, and its impact on global economies will continue to be felt until it has run its course–either naturally or through development of a treatment or a cure.

While there are reasons for optimism amid the crisis, it remains possible that the current predicament may persist for much longer than many analysts currently believe.

Still, there is no denying that the massive interventions by central banks and fiscal authorities worldwide have been supportive and stimulative–even if the effects are mainly psychological and affecting investor behaviors.

The US economy remains more dynamic than many others around the globe, but the country also remains vulnerable to a second wave of Covid-19 infections.

Some sectors are already responding strongly. Per a recent Financial Times story on the major banks:

Wall Street’s top five banks have posted their best quarter for trading in a decade after the coronavirus pandemic led to frenzied market conditions and radical interventions from central banks. JPMorgan Chase, Goldman Sachs, Morgan Stanley, Bank of America and Citigroup posted combined trading revenues of $33.4bn in the second quarter, their highest tally since the $33.7bn they made in the first quarter of 2010. The gains cushioned the blow of more than $20bn of provisions for loan losses on the banks’ income statements.

…“It was probably as good an environment as you could have,” said Carey Lathrop, co-head of global markets at Citi and a 32-year trading veteran. He described two key factors: clients rapidly adjusting their portfolios to deal with fast-changing economic forecasts, and the huge bond-buying programmes launched by the US Federal Reserve and other central banks — which had also slashed interest rates.

…Traders said that the Fed’s promise in March to buy sovereign bonds in unlimited amounts and to buy corporate bonds for the first time, followed by a pledge in early April to buy riskier credit, helped to stabilise the market. The actions changed investors’ mindset from “…‘how far can this go, how negative can it get?’ to ‘what assets should I be buying right now?’…”

Industrial metals (especially copper) are also pointing to optimism about a potential economic recovery. Per a recent Wall Street Journal article, by early July copper had rallied over 30% from its low in March, “…reflecting optimism about the potential for a sharp economic recovery, as China and Europe lead large parts of the world in easing lockdown measures. That has helped erase most of the commodity’s losses for this year.”

Note: through 3-July-2020. Sources: WSJ and LME

The article continues: “…A revival in Chinese economic activity in recent months has helped propel copper prices higher. The commodity is particularly sensitive to the Asian manufacturing powerhouse, as the world’s second-largest economy accounts for a large part of global demand for the metal. The reopening of major economies in Europe is also helping bolster demand for the industrial metal, analysts said.”

Note: through 3-July-2020. Sources: WSJ and Factset

Returning to the JP Morgan Midyear Outlook, they summarize the situation well: “…The range of possible outcomes related to the virus is wide; at opposite ends of the curve, possible tail risks include either a second wave in the Fall (a clear negative), or the development of an effective vaccine or treatment (a clear positive).”

Also, it is good to remember that markets don’t move in straight lines. So we are likely to see multiple stages of relief rallies and corrections in financial markets before a recovery eventually takes hold.

Stay safe out there!

It is no exaggeration to say that the biggest uncertainty facing us all at the start of the third quarter is still the outlook for the Covid-19 virus. Without knowing how the virus will play out, it is very difficult to know what to expect for the rest of 2020.

Despite the uncertainties, our entire team here at Anson Funds remains committed to navigating the stormy seas that lie ahead. While regulations prevent us from disclosing the specific performance of our various funds on this public blog, we can say that we are pleased with both the performance of our funds and with our overall risk management during the volatile first half of 2020.

Going forward, we intend to keep doing what has worked for us so far: continue to invest carefully, mindful of the uncertainties and disruptions we will likely face for the rest of 2020 and beyond.

During the first quarter of 2020 the entire world (and almost all markets) experienced a massive and unprecedented crisis, the likes of which has not been seen in modern times–the global pandemic known as COVID-19. As of the end of the first quarter, there is still no end in sight to this pandemic. This post looks at the expected effects of the pandemic across the following dimensions:

Health of populations – hundreds of thousands of deaths

Economies of all countries – grinding to a halt

Financial systems – including banks, payment systems, non-bank lenders, investment banks, broker-dealers, etc.)

Social systems – people’s day-to-day lives

Politics – not yet affected, but likely to happen once crisis stage passes

The COVID-19 pandemic arrived at a terrible time for global securities markets, given the instability and fragility of most markets

Markets spent the first seven weeks of the quarter continuing their multi-year climbs. Suddenly, right after making all-time highs in late February, markets began dropping on fears of the pandemic

In the space of just four weeks, major equity markets tumbled from all-time highs on February 19th to multi-year lows on March 23rd.

By March 23rd, the benchmark S&P 500 index had fallen to levels last seen in December 2016, over three years ago

The S&P 500 index fell over 34% from its all-time-high on February 19th to its low on March 23rd. It then rallied hard in the final week of March to end the first quarter down just under 20%

Commodities, especially bellwethers like oil and gold made huge moves during 1Q20, pointing to the massive stresses in global markets

Oil prices began dropping after the start of a price war between Russia and Saudi Arabia

As Russia and the Saudis failed to agree on production cuts, oil tumbled almost 70% from its recent high during the third week of January through the end of the first quarter

Gold reached new multi-year highs in early March before selling off (like all assets) in mid-March.

Gold also experienced unprecedented short-term swings during the quarter, including a huge sell-off in mid March

US dollar funding stresses also rose dramatically as borrowers and traders worldwide all scrambled to access the currency

Indicators of US dollar funding costs in FX markets have risen sharply, approaching levels last seen during the Great Financial Crisis (2008-2009).

One such measure is the so called FX swap basis, or the difference between the dollar interest rate in the money market and the implied dollar interest rate from the FX swap market

In recent weeks, the FX swap basis widened sharply, with the large negative basis reflecting a scarcity of dollar funding.

Initial Responses to Pandemic

As we are facing numerous unknowns, no one can honestly claim to have answers. Everyone is in a brand new world. Still, as of the end of the first quarter, here is how things stood:

Virus/health

As of mid-April, the USA already had the highest number of infected cases and the highest number of death from COVID-19

The good news is that the numbers for China, Italy, and Spain (the worst affected countries previously) all appear to have peaked and started to turn down. If the USA follows a similar path, hopefully the peak for the USA is only a few weeks away

However, no one knows for certain whether or not there will be new waves of infection cases once strict lock down rules are relaxed

Economies

The coronavirus crisis will exact the biggest toll on the global economy since the 1930s Great Depression, according to warnings from the IMF. In a report dated April 14th, 2020, the IMF predicted that its forecast for 2020 global GDP will fall 6%, from +3% to -3%.

The IMF’s sobering estimates expect the pandemic to leave lasting economic scars, with the economies of most countries emerging 5 per cent smaller than planned, even after a sharp recovery in 2021.

The IMF said the output loss would “dwarf” the global financial crisis 12 years ago. The global contraction this year will be so bad that only a handful of people in the world will have experienced a similar event in their adult lifetimes. The IMF had to look back 90 years to the 1930s Great Depression to find a deeper recession.

While avoiding some of the most pessimistic assumptions in the private sector, the IMF expects advanced economies to contract by 6.1 per cent and emerging economies to shrink by 1 per cent this year. Positive growth is still expected in India and China.

Even after the sharp rebound which the IMF forecasts for next year, output is still expected to be 5 per cent lower in 2021 than expected in the IMF’s forecasts from October last year for advanced economies.

“This is a deep recession. It is a recession that involves solvency issues and unemployment going up substantially and these leave scars,” said Gita Gopinath, the IMF’s chief economist.

Emerging economies are forecast to perform better as a whole, but that is boosted significantly by China which is expected to see output in 2021 just 1.4 per cent lower than the IMF forecast six months ago.

If extensive lock downs continue into the second quarter of the year and COVID-19 returns in a milder outbreak in 2021, the overall economic hit would be twice as large, the IMF estimated.

Still, the IMF’s economic forecasts for 2020 are not even as dire as many private sector forecasts.

Financial system

The US central bank, the Federal Reserve, has acted faster and more aggressively than any other time in its almost 107 year history to address the crisis

It has re-launched every tool that it used during the GFC in 2008, but it has started faster and the facilities are much larger in 2020

It has also launched new tools and facilities, never used before

The US Treasury and Congress are also launching new fiscal actions, with the Treasury planning to work together with the Fed in setting up Special Purpose Vehicles (SPVs) to facilitate and accelerate spending

Social systems

A recent Bloomberg story summarized the situation well:

Social unrest had already been increasing around the world before COVID-19 began its journey. According to one count, there have been about 100 large anti-government protests since 2017, from the gilets jaunes riots in a rich country like France to demonstrations against strongmen in poor countries such as Sudan and Bolivia. About 20 of these uprisings toppled leaders, while several were suppressed by brutal crackdowns and many others went back to simmering until the next outbreak.

The International Labor Organization has warned that COVID-19 will destroy 195 million jobs worldwide, and drastically cut the income of another 1.25 billion people. Most of them were already poor. As their suffering worsens, so do other scourges, from alcoholism and drug addiction to domestic violence and child abuse, leaving whole populations traumatized, perhaps permanently.

In this context, it would be naive to think that, once this medical emergency is over, either individual countries or the world can carry on as before. Anger and bitterness will find new outlets. Early harbingers include millions of Brazilians banging pots and pans from their windows to protest against their government, or Lebanese prisoners rioting in their overcrowded jails.

After this first wave, it is very likely that there will be additional waves to this crisis.

Also likely that we start seeing some of the political ramifications of what’s happening right now.

Can’t have a dislocation of this size in financial markets and the real economy without having very material political repercussions both within countries and then between and among different countries.

So the question is how will all this affect corporations and consumers?

How do markets respond? The truth is we don’t really know. There are a number of different directions that we could go in. Below we look at optimistic, muddle-through, and dangerous scenarios for the future:

Optimistic scenario

All of this intervention really does fill the hole that was left by this massive decline in people’s incomes and corporations’ revenues

Somehow, we push through this psychological disruption and this current stay-at-home crisis and the economy can restore balance reasonably quickly. And we just kind of carry on.

There probably needs to be a treatment (or treatments) for COVID-19, hopefully followed by a vaccine. Markets are currently pricing in this type of scenario. Right now, in early 2Q20, equities are not down that much, considering the economic and financial chaos. The equity market appears to be trying to look through this crisis to the other side.

Other scenarios – versions of ‘just trudge through this’

Consumers and corporate CEOs are so reluctant to spend money or make capital investments that we just get stuck in a bit of a depressionary-type bunker mentality by all the major economic actors

This existing depression that we’re in right now turns into something that’s just more chronic

While the policy makers feel that their tools are sufficient to get us out, it’s just much harder than expected to reverse that type of bunker mentality that people grind themselves into.

More dangerous scenario

Could lead society to start looking for all kinds of scapegoats and could lead to just darker scenarios.

Economic disruptions

Higher taxes

Low interest rates for a long time

Reversal of off-shoring

Geopolitical disruptions

De-globalization

Would destroy a lot of capacity, just in that if we make a decision as a society that we want to just essentially trash our international supply chains, that’s just a huge productive capacity that we’ve built up over the last 20 years.

If we decide after this crisis that we need to build a lot more redundancy here in the US, then by definition we have destroyed a lot of capital and productive capacity and we will need to rebuild it here.

And so the economy that starts to get its legs back with the decision to have to rebuild productive capacity domestically, that would be a very strong case for a really material inflation.

Less international cooperation

Political disruptions

Rise of leftist politics

Slowdown of immigration

Inflation becomes a consideration that we all need to think about.

An environment where the government throws a lot of money at the economy and people just save it, that’s not a particularly inflationary-type setup. And I think it’s probably where we are right now.

But in an environment where the central banks and governments throw a lot of money at the economy and things really start picking up quickly, then inflationary risks become a lot more likely

But the big inflations of the world are really caused by a major decline in supply combined with some type of monetary mischief by countries.

The question is what is the big disruption? It’s supply. Historically, wars destroy supply, the ability to produce things. When you combine that with monetary mischief or money printing, you get a lot of inflation.

It is very possible that this eleven-year period of rising equity prices is over now. Since the Fed launched QE and related programs in early 2009, markets have been on a slow-and-steady climb. But in many respects, the US has been the outlier already for the past few years.

Japan is still essentially where it was in the late 1980s.

European stocks are back to where they were twenty years ago.

The US has really been the only major market that’s really moved.

There have been a couple of other markets, but in terms of the really big major markets, the US has been a huge outlier.

Very likely that this period is in the process of ending.

Possible that future policies will be much more friendly toward labor, much less friendly toward capital.

And all that will impact the financial markets in a really profound way.

And, as pointed out in a recent blog post by Boston University professor Perry Mehrling:

…[O]nce everyone finally moves to recovery mode, we will not be restarting the BC (before coronavirus) supply chains because we have learned from the crisis about their fragility. Supply chains of the future will be more resilient, with plenty of inventories and redundancies. And certain industries deemed vital for national security will be on-shored. The real challenge facing us is thus the challenge of reconstruction, which I take to be about resisting the drift to autarky and nationalism and embracing instead the challenge of re-globalization.

Here at Anson Funds, we remain committed to navigating the stormy seas that lie ahead. While we cannot discuss the specific performance of our various funds on this public blog, we can say that we are pleased with both the performance of our funds and with our overall risk management during the volatile first quarter of 2020.

Going forward, we intend to continue to invest carefully, given the uncertainties and disruptions we expect to face for the rest of 2020 and beyond.

{kind=link}

{kind=link}